This article is an onsite version of our Chris Giles on Central Banks newsletter. Premium subscribers can sign up here to get the newsletter delivered every Tuesday. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

Until the post-pandemic inflation, central banks predominantly used forecasts of prices as the main guide to setting rates. These would come from a suite of economic models. Ultimately, the data was paramount, but because it was rarely that different from the forecasts, officials could genuinely anticipate the future with reasonable accuracy.

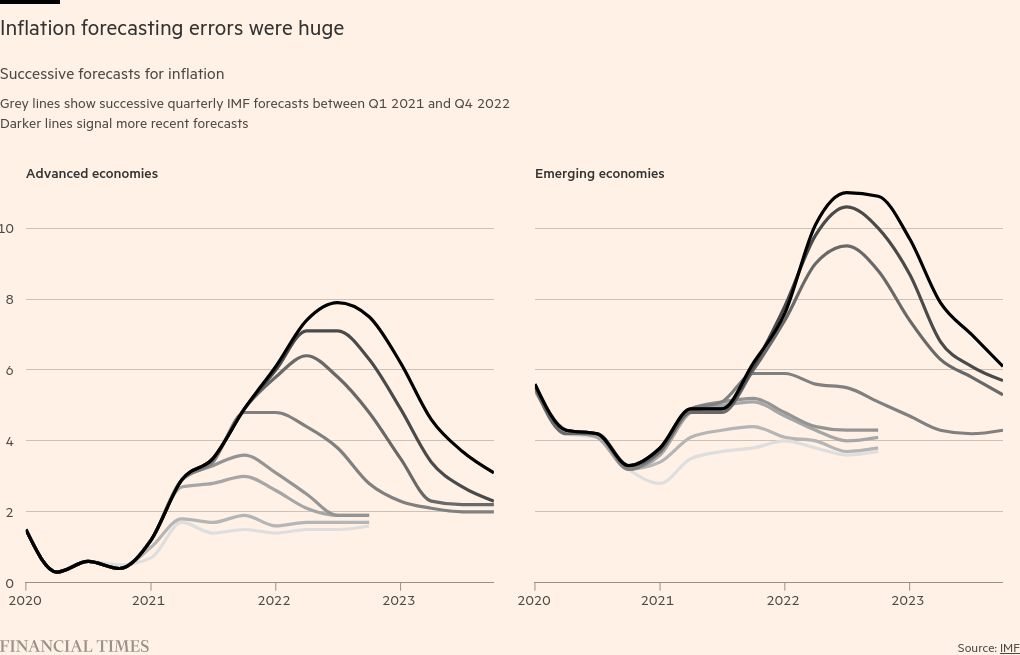

That changed in 2021 and 2022. As the chart below on IMF inflation forecasts and the emerging reality in those years shows, whether it was for advanced or emerging economies, inflation was much higher than expected and the models failed.

These facts applied almost everywhere and have spawned vast amounts of rather unsatisfactory research seeking to explain what happened.

Central banks felt they had to act by tightening monetary policy for fear of allowing inflation to spiral, but they were flying blind, having to set interest rates more as a reaction to inflation figures than in response to their analysis of where prices were heading.

Although officials generally loath looking at past decisions, the Federal Reserve and the European Central Bank have at least accepted that they were probably late to recognise the dangers and had to become more data-dependent. The Bank of England characteristically adopted the same solution without accepting it had made any errors at all.

We have now moved well into the second half of 2024 and the forecast world has changed again. Central bank predictions have become much more accurate.

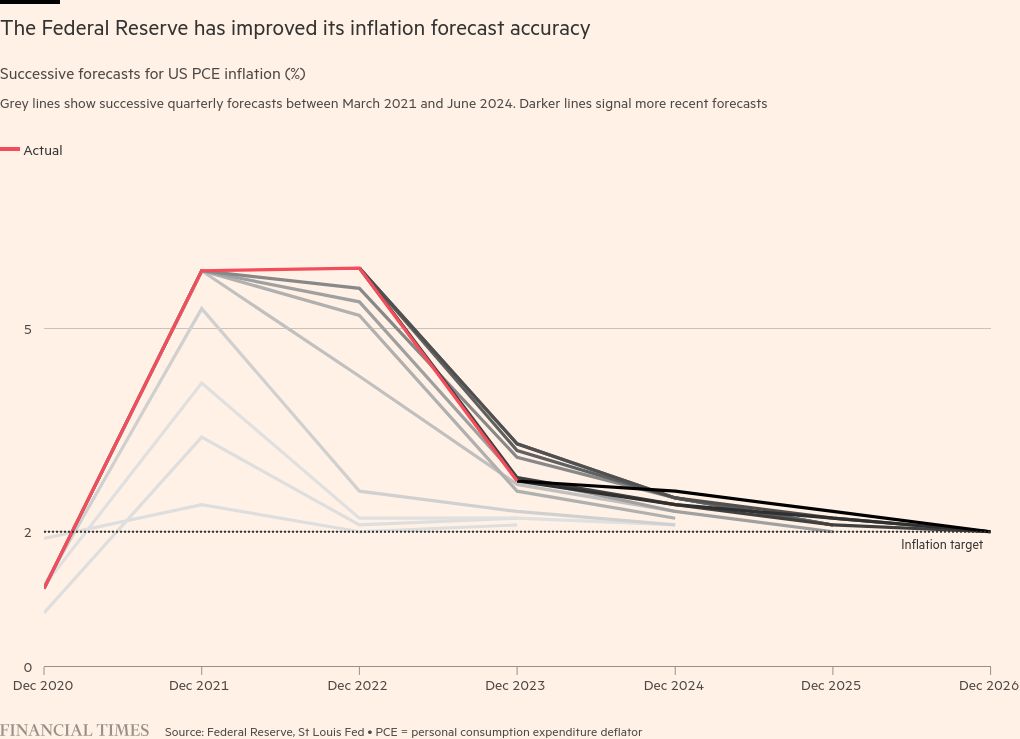

The median forecasts of the Federal Open Market Committee members apply only to the fourth quarter of each year and the errors for Q4 2021 and Q4 2022 are very large, as shown in the chart below.

In March 2021, FOMC members expected inflation that December to be 2.4 per cent and it was almost 6 per cent. Similar errors were made for 2022, but by 2023, inflation had come down and the Fed’s forecasting ability had improved. Errors now are small.

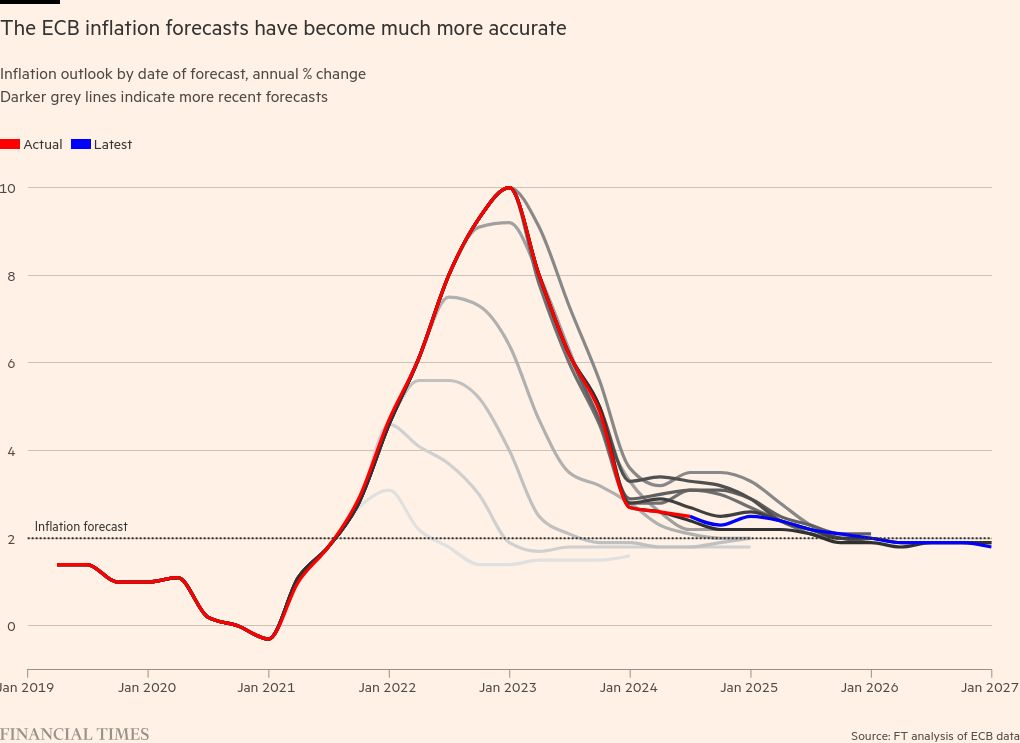

The ECB’s staff forecast is more detailed and shows a similar pattern. They severely underestimated inflation, starting in late 2021 and continuing through 2022. Again, inflation has more recently been lower than forecast as much as it has been above.

This puts some of the very recent underestimates of inflation in context. For most of last year, central bank governors across most of the Eurozone would have happily settled for the current levels of inflation. It was just that everyone got a little over-optimistic and there has been disappointment with later inflation out-turns.

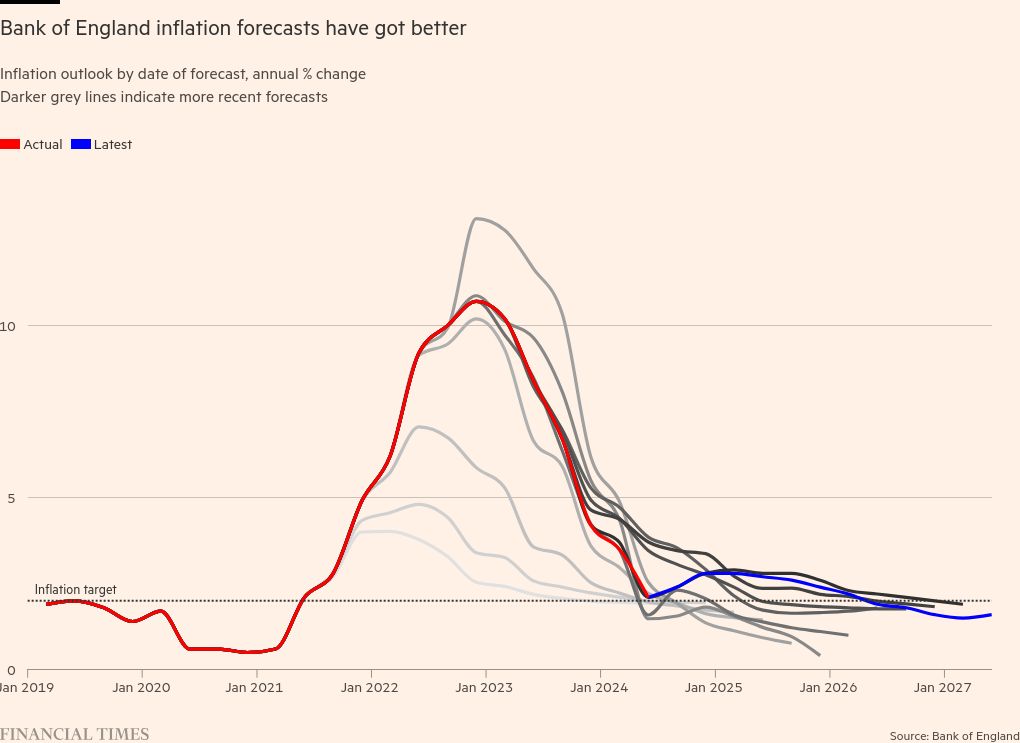

The same chart for the Bank of England tells a similar story. Huge underestimates of inflation on the way up (with one overestimate of inflation in August 2022 before the government capped energy prices) and then price rises have moderated more quickly than feared.

Although some past predictions expected inflation to fall away faster, primarily because the BoE also expected a long recession, the forecasts have become much more accurate.

Response to improved forecasts

The question for central bankers is what to do with policy now that forecasts are objectively more accurate, even if inflation is not quite back to target.

The answer clearly is not to trust forecasts entirely, nor to be purely led by the latest inflation figures, which themselves are prone to measurement error and give little indication of the future.

So far, the ECB has tried to merge data dependence, its forecast and an assessment of the transmission of interest rates to the economy. Christine Lagarde, its president, modified that slightly this month, saying it will base its assessment on “data, not data points”. This conveys a sense that the ECB will ignore occasional unwelcome data points as long as the disinflation process is broadly on track.

But there is some disagreement over the interpretation of these remarks in the ECB’s ranks. Philip Lane, chief economist, produced slides recently showing wages in line with the bank’s expectations, while Isabel Schnabel, another executive board member, said in the past week that repeated disappointments in services inflation were sufficient for “taking a closer look” at the assumptions underlying the projections. Tension between these two officials on their assessment has been pretty common and is healthy (so far).

The US will have its chance to strike a balance between forecasts and data on Wednesday, but with the data having been favourable of late (see below), Fed chair Jay Powell is almost certain to be comfortable with his current stance that he wants more “confidence” on the data before cutting rates but that they are growing closer.

The BoE and the Bank of Japan have the most difficulty in deciding which way to jump this week. The more confident they are, the more they will highlight forecasts not data and cut rates (UK) or raise them (Japan).

Graphs not pictures

I asked you last week what you thought the ECB’s picture below was describing. No one came close to the reality. Most people, with some reason, thought it was trying to convey a message of cutting rates carefully.

The truth is that the drawing is supposed to represent the following:

“We kept our interest rate unchanged

Our rates are still high, helping push down inflation. This is still needed because inflation is likely to stay above our 2 per cent target well into next year.

Pictures do not really help communication is my main conclusion from this.

The images do make sense if you follow all the previous incarnations of the same woman in the picture. You can see from a comparison with the June version that she is now further away from the rate cut. This is madness though. If pictures are supposed to help a less engaged audience, you absolutely cannot expect them to be following each incarnation of a random person carrying a percentage point symbol meeting by meeting.

July 2024

June 2024

What I’ve been reading and watching

-

Kamala Harris, now the presumptive US presidential nominee for the Democratic party, has never defined herself with an economic narrative. Colby Smith and James Politi report on what we know, concluding that she will champion the US middle class, continuing the economic policies of Joe Biden if she is elected.

-

One potential troubling problem for the US economy is the first signs of consumer weakness, while Russia has a consumer spending boom fuelled by a large government budget deficit and rising inflation on its hands.

-

Revolut finally persuaded the Bank of England to give it a UK banking licence, allowing it to offer products such as mortgages, in the same week as the ECB was preparing to withdraw the operating licence for Banque Havilland, the Luxembourg-based lender owned by Prince Andrew’s longtime financial adviser David Rowland and his family.

-

Some groundbreaking research on universal basic incomes was published last week. The findings make UBI even harder to justify than people thought, as I noted in a column.

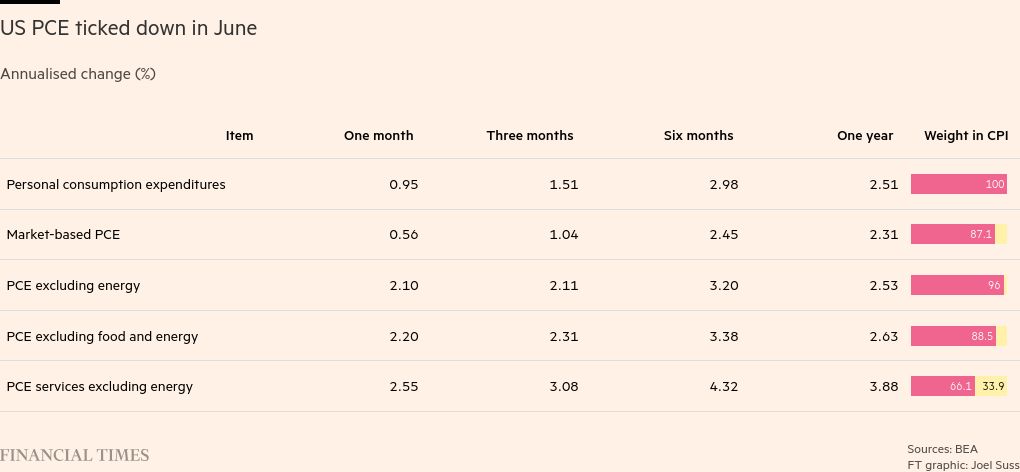

A table that matters

US inflation data on Friday was just what the Fed needs to indicate that it is gaining the confidence it needs to start cutting interest rates in September. The table below shows many variants of the personal consumption deflator with price rises close to target in June on all measures.

Annualised price rises over one and three months are under control, and market-based prices are now rising at substantially below target rate.

Recommended newsletters for you

Free lunch — Your guide to the global economic policy debate. Sign up here

The State of Britain — Helping you navigate the twists and turns of Britain’s post-Brexit relationship with Europe and beyond. Sign up here