Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Alphabet wants to spend on capital expenditures ($13bn in the quarter just ended). Alphabet wants to spend on dividends ($2.5bn). Alphabet wants to spend on buybacks ($16bn).

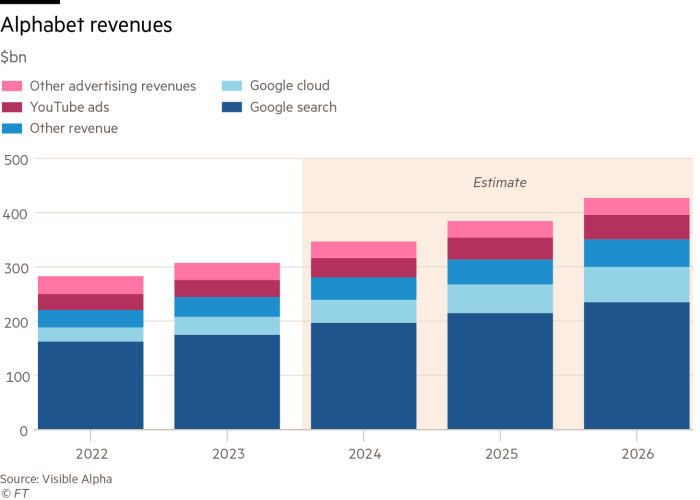

But how about M&A? Google’s parent reported healthy second-quarter results on Tuesday. Overall revenues were up 14 per cent. Search advertising revenues have not been dented by AI just yet.

Google’s cloud computing business, however, was benefiting from customers building up their AI capabilities, with revenue up 29 per cent. Cost cuts and redundancies helped keep operating margins above 30 per cent. And Google shares have benefited from the broader rotation into big technology stocks with its share price up almost a third so far in 2024. Its market cap is $2.3tn.

But in terms of what comes next, it is worth considering the group’s dealmaking (or lack of it). Dealmaking looks clumsy at the moment at Alphabet. Late Monday, Wiz, the hot cloud security start-up, said that it was abandoning deal discussions with Alphabet after rumours days ago pegged a buyout at $23bn — far more than the company has ever spent to acquire another. Wiz said that it would focus on reaching its near-term target of annual recurring revenue of $1bn while pursuing an initial public offering.

The Financial Times reported that members of the Alphabet board were concerned about provoking Joe Biden’s administration, which has in effect made blockbuster M&A impossible for Big Tech thanks to antitrust concerns. Microsoft had to go to court to defeat the US Department of Justice over its $75bn deal for Activision. Adobe eventually abandoned a $20bn deal for rival Figma.

Another possible Alphabet deal for the listed software company HubSpot, with a current market cap of $25bn, has also reportedly been shelved.

Google is already in a US federal court subject to a landmark trial over improperly leveraging its strength in internet search to block competitors. And even with $10bn of quarterly revenue in cloud computing, advertising remains by far Alphabet’s dominant business.

That in the long term might become vulnerable to AI, government regulation or enforcement actions. It is understandable that Alphabet would want to find other areas of growth for diversification. And the regulatory environment is unpredictable at best.

But the boardroom division, in an otherwise successful and well-managed company, about how aggressive to be in pursuing new opportunities only underscores the dilemma.