This article is an on-site version of our Chris Giles on Central Banks newsletter. Premium subscribers can sign up here to get the newsletter delivered every Tuesday. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

Five years ago, the US Federal Reserve launched a review of its monetary policy strategy, tools and communications, committing to another instalment “roughly every five years”. That time is now.

The main innovation in the 2019-20 review was to introduce flexible average inflation targeting (FAIT), which committed the Fed to a new target. If there had been “periods when inflation has been running persistently below 2 per cent”, the central bank would target “inflation moderately above 2 per cent for some time”.

The wording was explicitly designed to improve performance in a low interest rate world where policy had been constrained by the zero interest rate lower bound. To this end, the Fed also said it would worry about shortfalls from maximum levels of employment rather than deviations from it.

As if on cue, Christine Lagarde also announced last week that the European Central Bank would undertake an “assessment” of its 2020-21 strategy review “reasonably soon”. This comes after the Bank of England’s slightly underwhelming review undertaken by Ben Bernanke earlier this year.

Fate of FAIT

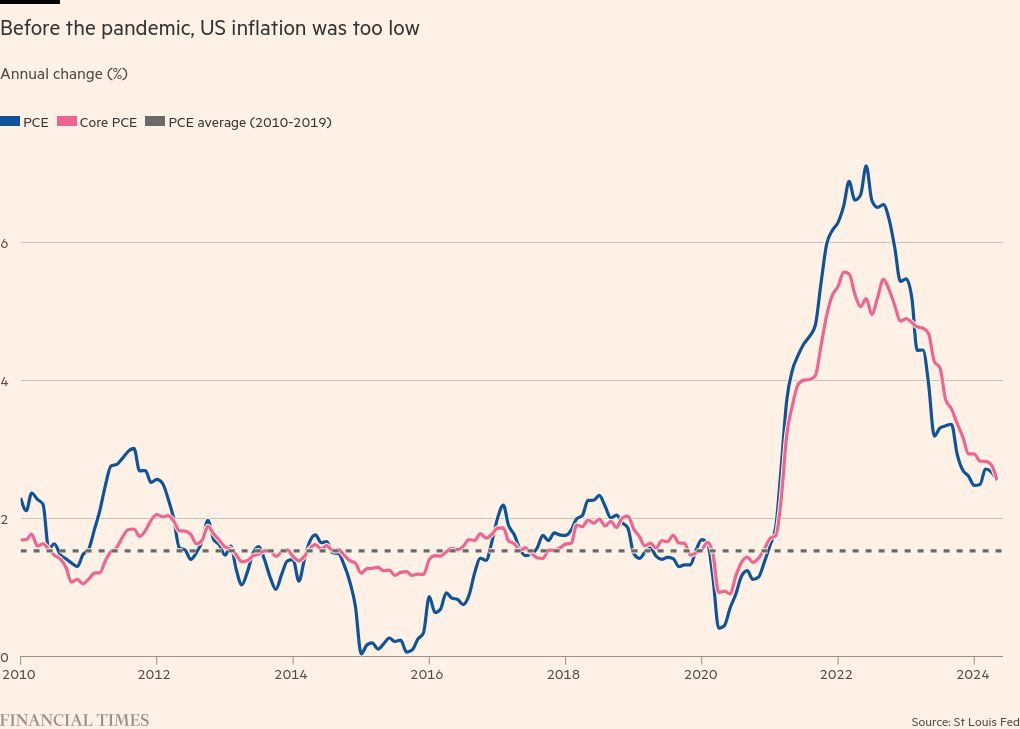

There is no doubt that in 2019-20, the Fed thought it had a problem of low inflation. Between 2010 and 2019, its preferred measure of inflation had averaged just over 1.5 per cent, well below its 2 per cent target, and it had regularly been constrained by interest rates sitting at their lower bound close to zero.

The review committing the central bank to a flexible average inflation target put a clear asymmetry into US monetary policy. If inflation overshot the target, that was a bygone that would be treated as a bygone; if it undershot, as it had in the previous decade, bygones would not be bygones. The Fed would be slower to raise rates, allowing an overshoot and this would be written down explicitly in the central bank’s statement on longer run goals and monetary policy strategy.

The last thing anyone expected was that the next five years would be an inflationary period and the Fed would be accused of being late to act. So, a big question now is whether FAIT was to blame?

This matter was discussed extensively at a Brookings Institution conference in June and the main findings have been published in a new Brookings blog. In it, Don Kohn, former vice-chair of the Fed, said the central bank should produce a framework that is “robust to a variety of circumstances” — periods of high inflation, as well as the ZLB — and not “just aimed at what we’ve recently lived through”.

This is unarguable.

But it does not quite answer the question whether FAIT was to blame. Speaking to Krishna Guha, vice-chair of Evercore ISI, I agree with him that it is almost impossible to blame FAIT for most of the inflation the US and others experienced. “The policy regime was not the first order problem here, it was supply shocks,” he told me.

The benefit of FAIT was to have an asymmetric response to the asymmetric problem that interest rates cannot fall below a lower bound.

Resolving this issue for the coming review, it seems that the Fed should maintain an asymmetry but be willing and able to act quicker if it is hit by a large inflationary shock. Therefore, it needs to be careful about binding itself in a low-for-long policy.

In the Brookings conference Brian Sack, of Balyasny Asset Management, sought to devise such a monetary strategy.

If you think you want a framework that’s robust to a variety of economic situations, a variety of policy challenges, I think the pieces of it that are robust are 1) inflation should average 2 per cent, and 2) policymakers should be aggressive enough to keep inflation expectations near 2 per cent.

Most people would agree with this. The Fed’s mistake was in not acting aggressively enough with big supply shocks and the Fed should think more about its interpretation of its current strategy.

In fact, and I hate to say this to Americans with a “not invented here” mindset, you might benefit from reading the ECB monetary policy strategy since it strikes the balance rather well. I’ve reproduced it below.

The Governing Council’s commitment to the 2 per cent target is symmetric. This means that we consider negative and positive deviations from the target to be equally undesirable.

When the economy is operating close to the lower bound on nominal interest rates, it requires especially forceful or persistent monetary policy action to prevent negative deviations from the inflation target from becoming entrenched.

Agreement on the 2% target

Neither the Fed nor the ECB will change the 2 per cent target. That would be grotesque and a sure-fire way of damaging credibility after the inflation we have just experienced and learnt how much the public hated even modestly elevated price growth.

A fait accompli

Regarding the ECB’s assessment of its monetary strategy, Lagarde made clear that the 2 per cent target was not going to change. “Not on my watch,” she said. She also insisted there would be no consideration of US-style dot plots for the ECB “given the experience that some of my colleagues have had of this element”.

This shows it is not just the US that suffers from a “not invented here” syndrome.

Improved communications

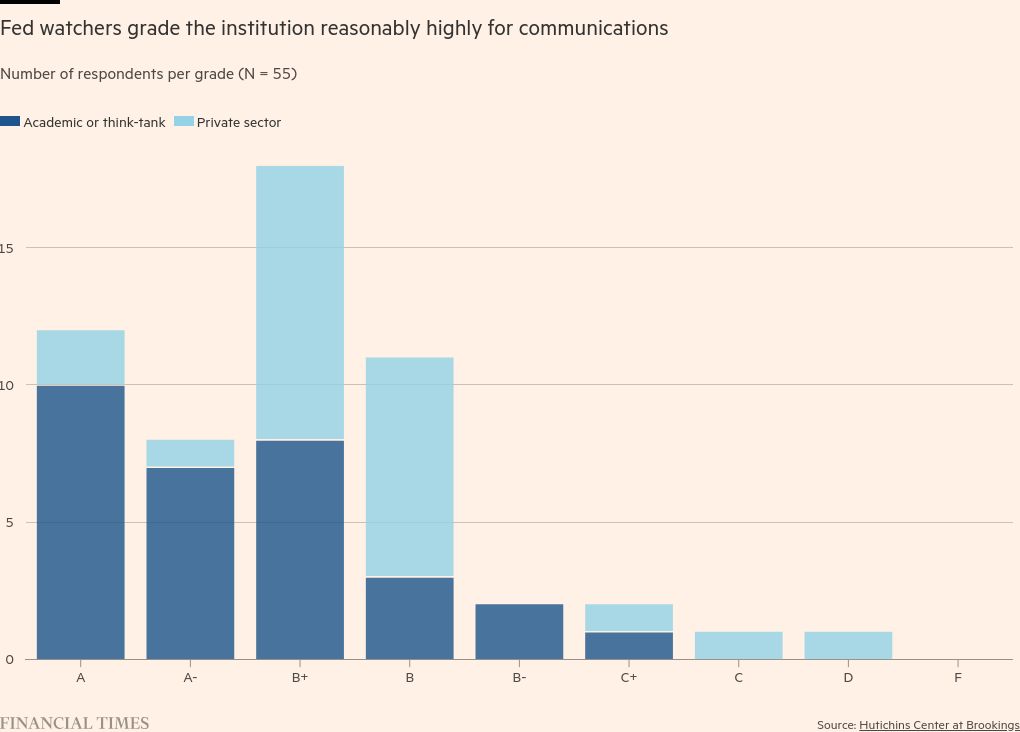

The Fed’s review will also examine its communication of monetary policy and strategy. That is welcome. The Fed already gets good marks here from academics, think-tankers and private sector respondents to a Brookings survey. However, I am not sure whether the Fed would be happy with a modal B+ score.

For me, good communication requires transparency — setting clear targets, showing your working, explaining your thinking, a willingness to course correct and, of course, explaining when you’ve done so.

It was clear from the Brookings conference that US Fed watchers were not delighted with its communications and it certainly had a rough time in 2021, when it stuck to the “transitory” explanation of inflation for too long.

But there is one aspect of the Brookings recommendations I could not disagree with more strongly. Communication with the public is important, it concluded, and to do this the Fed needed to learn from the ECB and BoE and pepper its websites with “pictures” to help explain monetary policy and strategy.

First, this shows a touching, but entirely unproven, faith in the public’s desire to visit the Fed, BoE and ECB websites. Second, it suggests pictures help.

I will leave you with a quiz. Do not visit the ECB website, but email me what you think the following primary picture from last week’s monetary policy meeting was trying to convey. I’ll provide the answer next week.

What I’ve been reading and watching

-

Analysts and European central bankers are increasingly sure that the ECB is set to cut interest rates again at its next meeting in September

-

Although all eyes are now on the Democratic Party, former president Donald Trump indicated in a Bloomberg interview that he would be angry about interest rate cuts before the November election. He said he would allow Jay Powell to serve out his full term, ending in 2026, if he was “doing the right thing”

-

China has cut its interest rates in the latest sign of concern about domestic demand

-

In a convincing piece of research, Sushil Wadhwani, a former BoE policymaker, found that UK bond prices contain an expensive “inflation premium” compared with others in the G7. The BoE and new government should take note

A chart that matters

The BoE has once again got itself into a bit of a communications pickle. At its May meeting, it said it would be data dependent and that meant interest rates would fall once services inflation and wage growth slowed.

At its June meeting, it cooled on data-dependence and said high services and wage inflation was explicable by one-off factors so they should not matter so much.

The latest data showed once again high services inflation and mixed wage data, and markets now expect it to become data dependent again.

This might be a time to believe the forecasts rather than the data. The CPI services overshoot in June was limited to a volatile hotel price component and early indications of median earnings growth have plummeted. For sure, there is a massive base effect in the chart below, but it shows the UK data is far from conclusive.

Recommended newsletters for you

Free lunch — Your guide to the global economic policy debate. Sign up here

The State of Britain — Helping you navigate the twists and turns of Britain’s post-Brexit relationship with Europe and beyond. Sign up here