On the High Street in Hungerford, a historic market town about an hour west of Reading, is Nigel Montgomery’s stamp and coin shop.

He has traded precious metals for about 50 years, but has never seen a gold rush like this: the price of a troy ounce, the unit used to weigh precious metals that dates to the Middle Ages, hit an all-time high this month, above $2,400.

“We’ve never seen so much retail demand as we are seeing at the moment,” says the 67-year-old. “I’ve been through various gold and silver booms since the 1970s — we’re seeing a more sustained, stronger and genuine rally.”

Investors have snapped up tax-free capital gains in gold sovereign and Britannia coins to hedge their portfolios against inflation and any escalation of conflict in the Middle East. So much so that Montgomery is continuously having to replenish his stock.

But the origins of this gold rush are thousands of miles from Montgomery’s town — and far from the historic global trading centres of London, Zurich and New York — in Beijing and Shanghai.

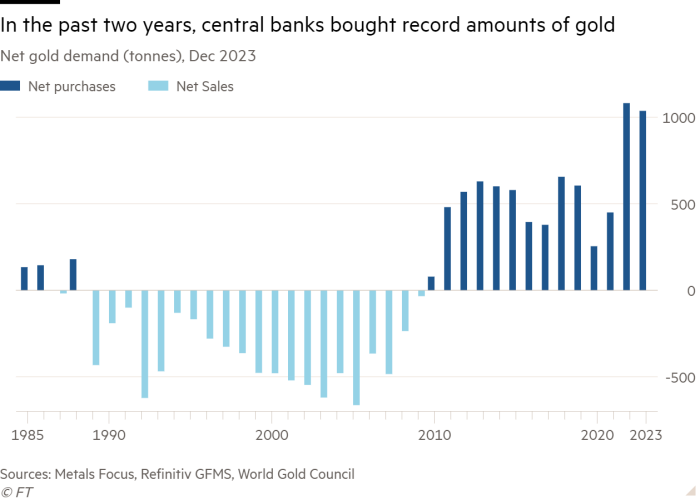

The People’s Bank of China led record gold purchases by central banks in 2022 and 2023, collectively buying above 1,000 tonnes each year, as emerging markets sought to diversify their reserve holdings away from the US dollar, which was weaponised by Washington in sanctions against Russia after its invasion of Ukraine.

Chinese retail investors have amassed gold as other investments from property to local equities turn sour. Chinese hedge funds and other speculators have also piled in.

“This rally has Chinese characteristics written all over it,” says John Reade, chief market strategist at the World Gold Council, an industry lobby group. “Everything leads back to different actors in China.”

While punters in Hungerford and at Costco stores across the US go gaga for gold, the western investor has, by and large, sat on the sidelines of gold’s latest rally. Gold-backed exchange traded funds (ETFs) have continued to experience monthly outflows, while bar and coin demand has been abysmal in Germany, typically the world’s third-largest market.

Andreas Habluetzel, chief executive of Degussa Goldhandel, Europe’s largest gold dealer, which owns London’s Sharps Pixley, says the cost of living crisis and stubborn inflation is driving customers to sell.

“We all want to keep the same lifestyle: sending your kids to good schools and owning two cars. When we talk to the middle-income people they are liquidating as they need money,” he says.

That creates a dilemma for the western armchair investor. Gold has rallied some $600 per troy ounce since conflict erupted between Israel and Hamas in October, yet the staggering rise is widely seen by analysts as disproportionate to the gold price’s usual drivers: real rates on US Treasuries, the dollar and ETF flows.

“This is not the behaviour of gold. It’s more or less the behaviour of crypto,” says Habluetzel.

When the asset is so volatile, should investors rely on it as a haven asset? And if the market’s centre of gravity is shifting to a set of investors in China with a fundamentally different set of concerns to your own, should you bank on backing bullion?

From a tactical perspective, gold’s sharp rise could make it poised for a sharp correction, having already fallen about $50 this week, making it a dangerous entry point.

But others argue gold has a cohort of buyers waiting in the wings for any dips to pile into gold — including western ETF investors that have not participated yet. Deutsche Bank analyst Michael Hsueh says that it is likely that “any profit-taking by early investors would be replaced by investment from those who have so far not participated in the move”.

Looking further out, the question for investors is whether they believe the global monetary system is at the early innings of sweeping transformation. That might be a new era of persistent inflation that erodes the purchasing power of fiat currencies and great power competition that increases gold’s share of reserve assets at the US dollar’s expense.

Max Belmont, portfolio manager of the Gold strategy at First Eagle Investments, an asset manager, says that gold is “sniffing out” mounting concerns over the sustainability of global debt levels.

US debt increases by about $1tn every 100 days or so with interest rates at their current levels, while investors fear Europe could struggle to manage debt levels if Donald Trump enters the White House and pushes for Nato defence spending to rise. The IMF warned this month that the US, China, Italy and the UK “critically need to take policy action” on debt. Neither US presidential candidate shows much sign of wanting to rein in spending.

Nicky Shiels, precious metals analyst at MKS Pamp, a Swiss refinery and trader, says surging gold prices anticipate a “big regime change the west is going through”, from erosion of US dollar purchasing power, higher-for-longer inflation and a multipolar world.

When it comes to US debt, she says the market has grown increasingly convinced that the Fed may cut interest rates even if inflation roars higher in order to reduce the interest payments that the US government is servicing (the Fed is independent of the Treasury).

“This is it: two decades of easing monetary policy coming to a head,” she says.

On the other hand, emerging market central banks and sovereign wealth led by China, Russia and the Middle East are buying gold after the US sanctioned billions of dollars of Moscow’s reserves held in US bonds.

“It’s the dollar losing utility as an asset to store trade surpluses,” says John Hathaway, managing partner of Sprott Inc, a Canadian asset manager specialising in metals. Gold has traditionally tracked real rates of US Treasuries but he adds that “the Fed’s policies may not matter anymore to gold prices” given the new club of buyer’s motivations.

And Chinese investors are taking cues from their own central banks’ purchases. “An awful lot of private wealth is going to be running into gold as there’s nothing else to buy: property sucks, equities lose you money, cash in the bank is paying nothing and they can’t get the money offshore,” says Adrian Ash, director of research at BullionVault, an online gold marketplace.

But others say geopolitical risks, the dollar’s demise and debt concerns are over-egged.

“The world is not nearly as risky as [in] 1980,” says James Steel, chief precious metals analyst at HSBC, when gold hit its inflation-adjusted record high well above $3,000 per troy ounce.

For retail investors concerned that they missed riding the wave of frothy gold prices, one option could be gold mining equities.

Valuations of the world’s gold producers, led by Newmont and Barrick Gold, have rarely been as heavily discounted in the past 40 years versus the gold price as they are now, according to asset manager Schroders. That has made the gold mining sector’s collective valuation at roughly $300bn no bigger than Home Depot, the US DIY retailer.

The theory is that lofty gold prices will feed through to higher margins when gold producers next report earnings, sending share prices shooting up.

“It’s a different risk-reward. If gold prices double then you should get a bigger increase in your margin,” says Robert Crayfourd, who manages the Golden Prospect Precious Metals fund at CQS, an asset manager.

Jim Luke, fund manager at Schroders, wrote in a recent note that “dismal western sentiment” on gold and poor operational delivery by the sector’s leading companies were behind the low valuations.

“It is not hyperbole to say the sector could rally 50 per cent and still look inexpensive,” he says.

Gold mining equities face structural challenges from their ESG credentials, as they play little role in the energy transition, rising political risk in cash-strapped developing nations from Mali to Mexico and declining reserves.

More troubling, however, is that this gold rally has been driven by the Chinese central bank, retail investors, asset managers and funds for whom western gold mining equities hold little appeal.

Investors have been deterred by the sector’s inability to tame cost inflation from vital inputs such as fuel, explosives and cyanide in the past couple of years and overspending during previous booms. Fund managers want to see proof that margins will march higher.

John McCluskey, chief executive of Alamos Gold, a mid-sized Canadian gold producer, says that the tech-led run for equity markets, with the Dow Jones breaking above 38,000, makes it hard to call when gold producers will get a look in.

“‘The party is going full tilt. I think I’ll go home to check the gas is on’ — you’re not going to do that now. ‘I’ll stick it out and put it in these gold funds that haven’t performed well for 10 years’ — you don’t do that,” he says. But, he adds: “When they see the margins then they will buy those equities.”

Jason Todt calls himself one of the new breed of “retired gold bugs” who are partying hard.

After the global financial crisis, the manager of a car dealership in Missouri spent $100,000 from a property sale on gold. Had the 47-year-old held on to all of his bullion until now, it would be worth $120,000. Instead, Todt earned $1.5mn by selling $65,000 of his gold hoard in 2017 to buy bitcoin and other assets, enabling him to retire early in 2020, meet his Ukrainian wife and travel the world in a sailboat.

“It has taken seven years to get a 100 per cent return on gold when you can do that in bitcoin in a year,” he says.

Todt’s situation highlights the pull for many investors of potential mega-returns through cryptocurrencies, AI and tech stocks over the pursuit of wealth preservation.

Laith Khalaf, head of investment analysis at AJ Bell, warns that even for those trying to cling on to their wealth, gold often fails to fulfil its “safe haven” reputation because it is volatile and trades sideways or downwards for long periods of time.

“It shouldn’t be a big part of your portfolio,” he says. “No more than 5 per cent.”

But the wealthy of the world appear to disagree. US funds, family offices and asset managers are increasing gold’s allocation within their portfolios to 10-15 per cent, up from 5-7 per cent, says Habluetzel of Degussa.

That is underpinned by gold’s long-run ability to preserve wealth — if bought at the right time. Since 1970, when US President Richard Nixon untethered the dollar from gold, bullion has produced an average return of just below 8 per cent a year, says Peter Clark, a retired fund manager.

For Montgomery in Hungerford, gold is a must-have insurance policy for investors to protect themselves against an end to the equity and crypto mania.

“If we had world peace and a more stable economy, gold would be steady or go down,” he says. “But the world isn’t a stable place. People have had a really good run on the stock markets and property prices have kept going up. What’s left? It’s gold.”