Receive free Mergers & Acquisitions updates

We’ll send you a myFT Daily Digest email rounding up the latest Mergers & Acquisitions news every morning.

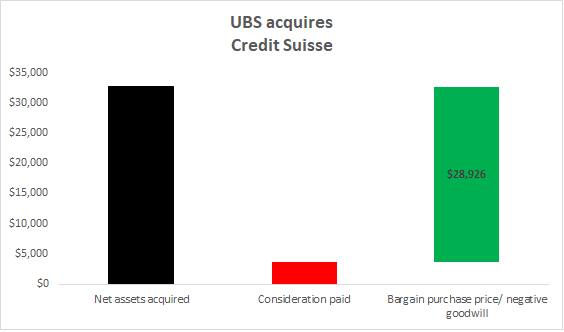

UBS’s second-quarter results last week included the effects of its June shotgun wedding with arch-rival Credit Suisse. Its $29bn profit was, by far, the single greatest three-month result earned by a bank.

This apparent “deal of the century” bore an accounting gain that in effect contributed all of those earnings. UBS scavenged the mortally wounded CS cheaply amid its potential collapse, a tie-up effectively demanded by the Swiss government.

With the books closed on that combination, we now have the official figures from quarterly reports and securities filings on all four of the major bank M&A rescues since the early spring crisis:

-

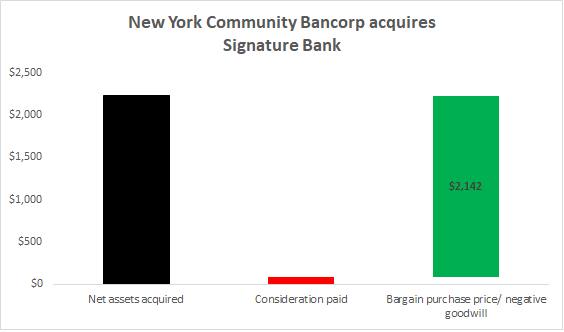

New York Community Bancorp/ Signature Bank (March)

-

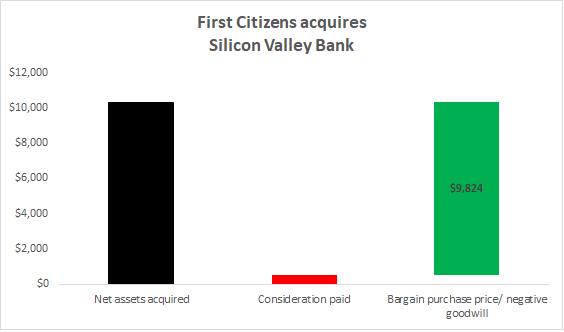

First Citizens/ Silicon Valley Bank (March)

-

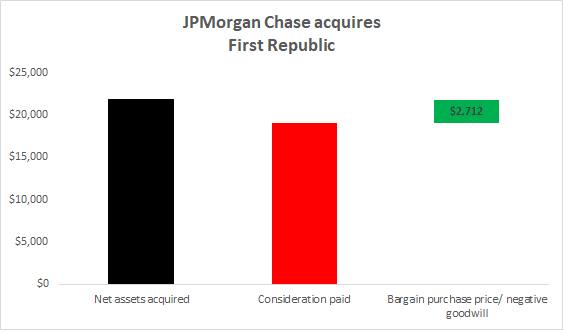

JPMorgan Chase/ First Republic Bank (May)

-

UBS/ Credit Suisse (June)

In any M&A deal, so-called purchase accounting will require the buyer to allocate the “excess purchase price” to all acquired assets and liabilities. Typically, the purchase price — the present value of future cash flows — will still exceed the revised balance sheet valuation.

That gap is known as “goodwill”. Often thought of as the je ne sais quoi of a company, yet goodwill is ultimately a mechanically-derived arithmetic output to ensure that the pro forma balance sheet does indeed balance.

But with this foursome of deals, the calculation is far more interesting. The transactions were extraordinary, with authorities desperate to find a buyer quickly and prevent broader contagion. As such, buyers could largely dictate the deal terms.

In each of these instances, the buyers took over the targets for an effective purchase price far less than the target’s book equity value, also called net asset value (the fair value of their assets less the fair value of their liabilities).

As such, the buyers did not need to raise their own costly and possibly dilutive equity in order to complete the deals. (In contrast, look at the recently announced merger between PacWest and Banc of California, a regular way transaction that requires a $500mn private equity infusion.)

The four deals each created the unusual “negative goodwill” since the net asset value exceeded the purchase price. Negative goodwill is the term under IFRS. Per US GAAP, the concept is known as a “bargain purchase gain”. In both instances, a gain is recorded and runs through the P&L to create income and then equity capital boosts at essentially no cost.

(Note that at the time of the deal announcements, the buyers each shared a preliminary calculation of their expected gains and now final purchase accounting largely confirms those initial figures.)

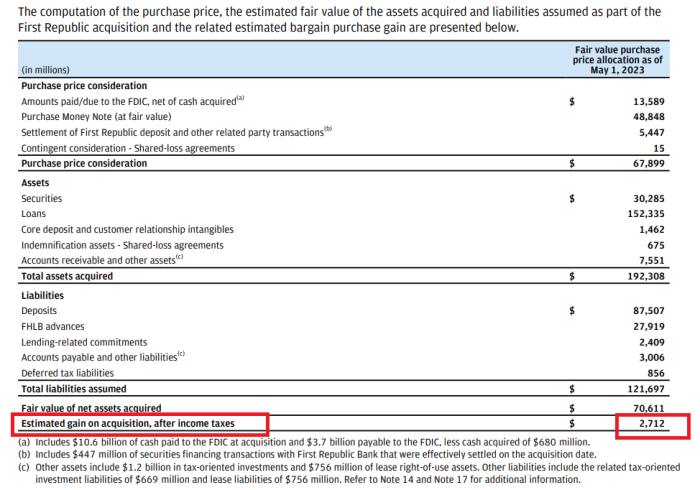

Here is an example, this one from JPMorgan/ First Republic:

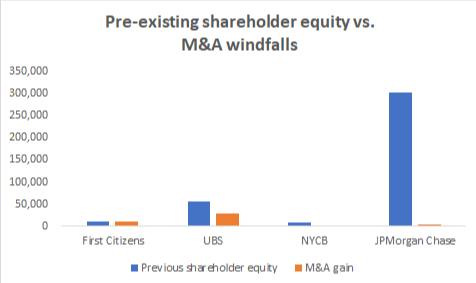

Alphaville has attempted to show the scale of the gains for the four buyers:

Those four green bars of bargain purchases prices/negative goodwill add up to $44bn in collective gain. Next we can see how big those gains were, relative to size of the banks, pre-deal, measured by their shareholder equity recorded in the previous quarter.

JPMorgan paid a relatively hefty price for First Republic, including a $10.6bn cheque to the FDIC and writing off the $5bn deposit it had made into First Republic earlier in the year. As such, its bargain purchase gain was less than $3bn for a bank with $300bn of shareholder equity.

First Citizens, a relatively small bank, doubled its equity base by getting most of Silicon Valley Bank for just $500mn.

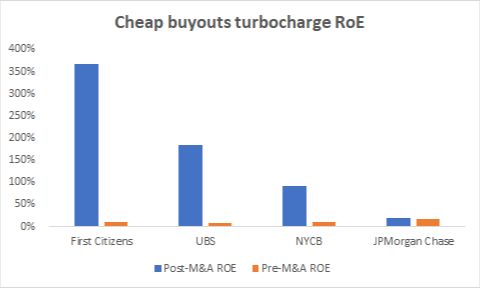

More precisely, return on equity (profits divided average shareholder equity) shows how efficient these deals were for the buyers.

First Citizens, UBS and NYCB each had RoEs in the previous quarter of between 9 per cent and 11 per cent. Then they each struck gold.

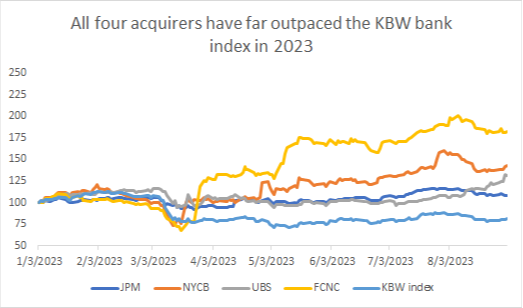

Accounting aside, what may matter most is how shareholders embraced these deals.

First Citizens stock price has almost doubled. NYCB is up 43 per cent and UBS is not far behind. JPMorgan is up just 9 per cent, indicating the small potatoes of FRB, but still is nearly 30 points ahead of the KBW bank index which is down nearly a fifth this year.

Exploiting the desperation of regulators meant mostly easy money for the buyers. The tough losses then have been imposed on previous shareholders of these moribund banks, their non-deposit creditors as well as the deposit insurance schemes that are funded broadly by the banking industry.

These failed banks had viable assets as these acquirers have demonstrated. Why the returns from those assets must be only captured by opportunistic parties remains a public policy question.