Receive free VinFast LLC updates

We’ll send you a myFT Daily Digest email rounding up the latest VinFast LLC news every morning.

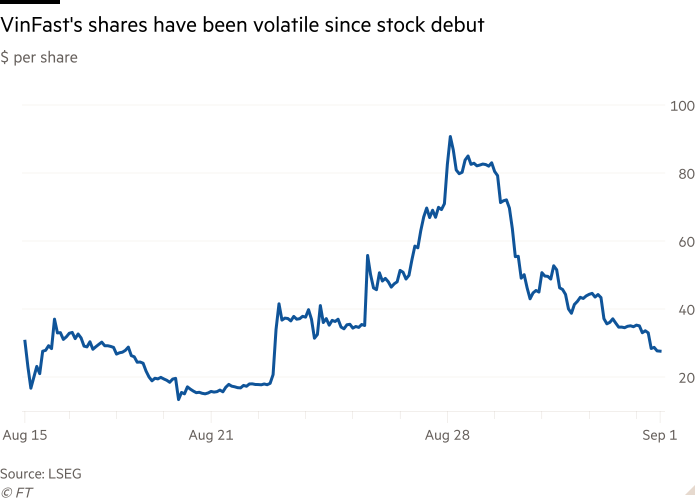

Just five years ago, Vietnam’s VinFast started to produce its first cars. Last week the electric vehicle maker was briefly valued at more than the combined worth of Ford, General Motors and Volkswagen.

In a remarkable stock debut, VinFast’s market capitalisation shot higher after its mid-August listing to a peak of around $190bn. The stock has since slumped and the market value fallen to $64bn. But that still it leaves more highly valued than General Motors ($46bn) and Ford ($48bn). Only Tesla ($785bn) and Toyota ($280bn) are worth more. That is despite the fact the company is only expecting to produce some 50,000 cars this year — a tiny number compared with the 5.9mn vehicles GM sold last year.

If you believe in efficient markets, it could be argued that investors are betting that VinFast, part of the sprawling Vietnamese conglomerate Vingroup, will rival Tesla and deliver huge growth. That would be a stretch, to put it mildly, particularly given how competitive the electric vehicle market is becoming.

More likely, it is valuation might be distorted by the tiny amount of the company’s shares that can be freely traded. The company’s so-called free float is just around 1 per cent with the rest held by Pham Nhat Vuong, Vietnam’s richest man. With such a meagre amount of supply of the shares, any demand can lead to sharp spikes in the share price.

This, of course, is not an uncommon phenomenon. Stock market history is replete with similar examples. VinFast’s surge came just a year after little-known Asian finance group AMTD Digital sold about a tenth of its shares in New York and subsequently skyrocketed 21,429 per cent. That briefly gave it a market value of $311bn. It is currently worth about $1bn. In Ireland, buying into such company during a spike was dubbed the “eejit trade” after Allied Irish Banks soared on more than one occasion in the decade following the 2008 financial crisis. When Dublin, which took over the lender during the crisis, divested some of its 99 per cent holding in 2017, the share price tumbled.

Before that there was Caesar’s Entertainment. In 2012, the US casino operator floated a 1.4 per cent stake in New York after a debt restructuring. They leapt 71 per cent on debut.

Such stories are dramatic in a world where most asset prices merely edge up or down on any given day. They’re a problem for regulators and exchanges, however. Too many and a market begins to look like a casino and raises suspicions of stock manipulation. But they’re not easy to prevent. Compare the examples here and they have little in common beyond their rocket episodes. That complicates the rulemakers’ job beyond, say, just raising the minimum free float needed to go public.

VinFast listed via a special purpose acquisition company — a so-called blank cheque vehicle, which raises funds and then looks for something to buy. Shareholders in Spacs have the option to cash out their holdings once the shell finds its target, or they can stay as shareholders in the merged, listed group. Investors holding 80 per cent cent of the shares in the Spac merging with VinFast redeemed their holdings — roughly in line with other recent deals. Such cancelled shares reduced VinFast’s free float.

“Most Spacs weren’t planning on having a really tiny free float, but if there’s a really high redemption ratio, they wind up [there],” says Jay Ritter, finance professor at the University of Florida. “Small free floats can result in manipulation, but actually most of the time the fundamentals that led to the high redemptions scare away investors and the price collapses.”

So how about mandating minimum free floats throughout a company’s trading life? Yet Hong Kong does that and is frequently criticised by market watchers. The city requires a public float minimum of about 25 per cent, or 10 per cent for larger groups. Those that fall short risk suspension and delisting. Suspensions have lasted years, trapping shareholders

“It doesn’t prevent stocks being cornered and ramped,” says David Webb, an independent investor advocate and long a critic of the rule. “[It] is based on the fundamental misconception that listed companies can control what their shareholders do. It’s supposed to be the other way around.”

There is one thing from Hong Kong, however, that regulators elsewhere could adopt more easily: slap a warning on very tightly-held companies, as the city’s watchdog does.

“Bourses such as the NYSE are cognisant that share manipulation is not so much the percentage of shares held in public hands, but the dollar size of the public float, and the number of public shareholders,” says David Blennerhassett, an analyst at Quiddity Advisors. “Suspending shares disadvantages innocent shareholders. The way to deal with this is by highlighting the issue.”

That’s a “buyer beware” approach that fits, in theory, with the general US model of disclosure. It’s hard to believe, though, that those trading VinFast or any of the other examples didn’t know about their stock scarcity issue soon after it began to soar. There are some elements of speculation that no regulator can fix.