Receive free Financial services updates

We’ll send you a myFT Daily Digest email rounding up the latest Financial services news every morning.

You may have noticed that private equity — cough — splits opinion. Even within the financial industry, lots of people think buyout artists are actually overpaid, overleveraged hacks whose mistakes are obscured by accounting gimmicks.

Dan Rasmussen at Verdad Advisors is very much one of the critics. His latest weekly email takes an interesting stab at examining whether the operational improvements private equity firms insist they make in their companies actually exist.

Spoiler alert: he doesn’t think so.

Investors should not take the industry’s word that PE firms are superior managers that drive superior performance at the firms they own. This is a myth akin to arguing that Republican presidents are better for the economy or Democratic presidents are better for the poor. It sounds plausible, but it’s very hard to prove with data. And investors should be motivated by data, not myths. As we have shown, this data is possible to obtain and analyse.

That analysis is easier said than done. The problem is that companies taken private no longer file regular public earnings, so there is a paucity of data. Still, many of them do issue debt, and in many of the bigger deals that means big public bond sales with accompanying financial data.

So Verdad compiled a database of 993 US deals between 1996 and 2021 where both pre-and-post acquisition financials were available. As Verdad admits, that’s a pretty small data set given the tens of thousands of PE deals that have taken place over that time. But it’s a snapshot, at least of the bigger deals.

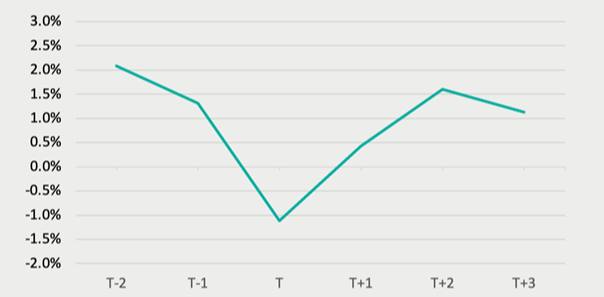

And, well, their performance hasn’t been great. Here are the charts showing revenue growth and earnings margins at PE-owned companies versus their listed peers, before and after their acquisitions.

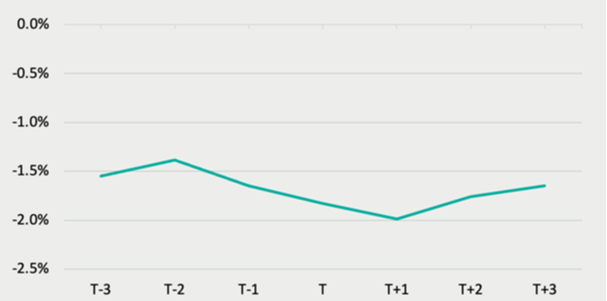

Here is what happens to capex and the ratio of profitability to their assets.

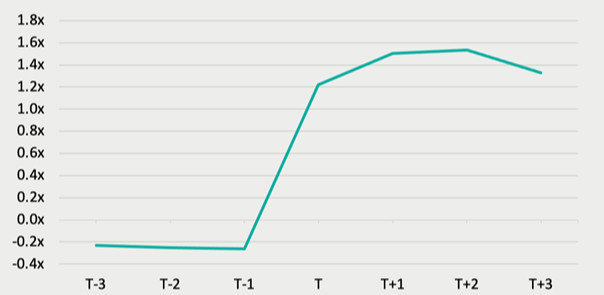

There is one area where the charts point upwards though, and it’s the one you’d expect: their debt-to-earnings ratio, relative to their peers.

This is evidence, in Rasmussen’s view, that private equity’s claims of improving the companies they buy is a “pervasive marketing myth”. He continues:

The industry mythology of savvy and efficient operators streamlining operations and directing strategy to increase growth just isn’t supported by data. Instead, there is a new paradigm to understand the PE model, and it’s very, very simple.

By and large, as an industry, PE firms take control of businesses to increase debt. As a result, or in tandem, the growth of the business and the rate of spending on capex slows. That’s a simple, structural change, not a grand shift in strategy or a change that really requires any expertise in management.

It should be noted that one of Verdad’s main products is selling a leveraged small-cap stock fund as a way to replicate PE returns without all the costs. Moreover, this study is not the most comprehensive we’ve seen.

The issue is that these kind of reports always show the average results, and the average is going to be, well . . . mediocre. There are always going to be some firms that can point to good results (or at least some good deals). Institutional investors seem happy enough, and they’re not all dummies.

But it’s hard not to think that a lot of them are going to end up disappointed if they gormlessly pencil in the kind of future returns the PE industry saw in an environment with four decades of falling interest rates.