Better deals: Higher interest rates mean people can buy more annuity income for their money – see latest industry average rates below

Over-50s remain dubious about annuities despite a recent recovery in the retirement income they can buy you after years in the doldrums, new research reveals.

One in five regard the products, which provide a guaranteed income until you die, as poor value.

Some 44 per cent of the older adults surveyed believe annuities are inflexible, and 45 per cent think they are risky in case you die earlier than expected, according to the research by Canada Life.

Annuities have been shunned for years due to poor rates and restrictive conditions, and after gaining a bad reputation on the back of mis-selling scandals.

Pension freedom reforms in 2015 prompted most savers to keep their funds invested and live off withdrawals instead.

However, the recent run of interest rate hikes mean annuity providers can afford to fund much more attractive deals, prompting a resurgence in sales.

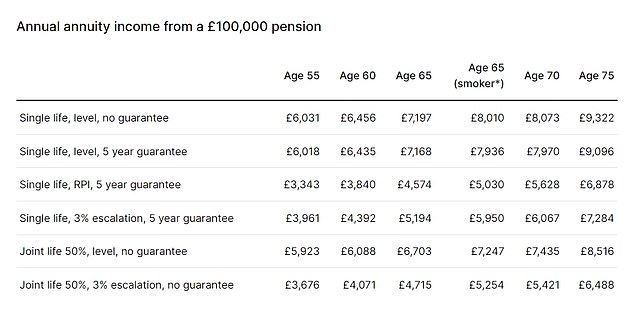

For £100,000, a healthy 65-year-old can now buy a retirement income of around £7,170 a year, with no inflation protection and a five-year guarantee period – protecting your cash immediately after purchase – a rate of almost 7.2 per cent.

For the same sum, the same person with a spouse three years younger could buy a joint life annuity with inflation protection but no guarantee that provides £4,720 a year, according to the latest industry average figures from Hargreaves Lansdown (see below).

Source: Average industry figures from Hargreaves Lansdown, 29 June

Canada Life says there are ‘common misconceptions’ about annuities, after surveying nearly 1,000 over-50s in the spring.

The insurer says annuity rates are at a near 14-year high after increasing by almost 50 per cent in the past 18 months.

And it adds that annuities can be flexible, with a ‘retirement account’ version that allows you to turn income off and on.

Canada Life says if you are worried that you will lose the purchase money by dying earlier than expected, you can buy a guarantee and value protection so income is paid to your nominated beneficiary.

The firm says its research also reveals ‘a real lack of awareness and understanding beyond the misconceptions’, because a significant number of people who said they were familiar with annuities sat on the fence and would neither agree nor disagree that they are good value or offer flexibility.

The pension freedom shake-up eight years ago prompted most savers to keep their funds invested, but this involves monitoring a portfolio and exposure to the risks of financial markets.

This is Money guides explore how to invest your pension, invest-and-drawdown plans versus annuities, and how to combine pension drawdown with annuities.

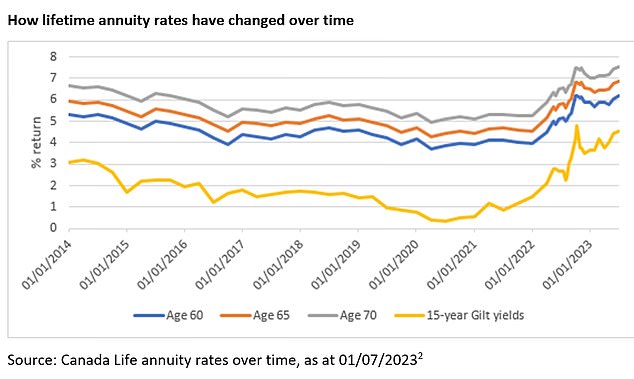

The chart above assumes a £100,000 annuity purchase price, a 10-year guarantee and no health or lifestyle factors

Retirement income director Nick Flynn says: ‘Annuities tend to be sold, rather than bought. This is exacerbated by the misconceptions that have built up around annuities as a product which has been out of fashion.’

But he says they are worth more than a cursory second glance due to significantly improved rates and longer guaranteed periods that are effectively a money-back option.