Receive free Mergers & Acquisitions updates

We’ll send you a myFT Daily Digest email rounding up the latest Mergers & Acquisitions news every morning.

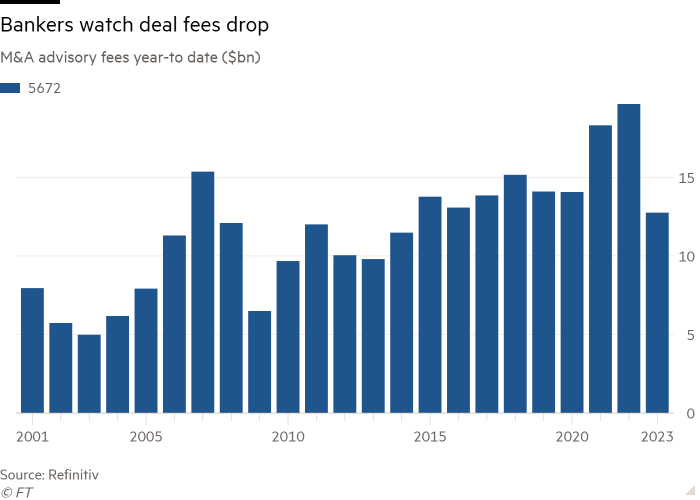

Investment bankers’ advisory fees have plunged to the lowest level in almost a decade as the industry suffers from a wave of job cuts because of a prolonged slowdown in deal activity.

Fees for completed mergers and acquisitions globally plummeted 35 per cent in the first half of the year to $12.8bn compared with 2022, the lowest level since 2014, according to data provider Refinitiv.

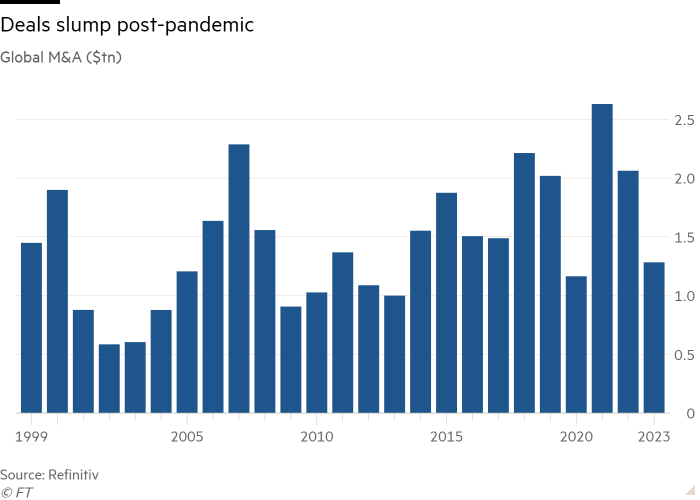

Global M&A fell 38 per cent to $1.3tn in the first half, the lowest deal volume since the start of the pandemic in 2020, as higher rates, stricter antitrust enforcement and geopolitical tensions hit the market.

Transactions driven by private equity groups, typically a key driver of dealmaking, also tumbled. Global private equity-backed M&A activity fell to $263.3bn in the first six months, down 51 per cent compared with last year.

Deals between private equity groups have been hampered by a number of factors including rising debt costs, concern over the economic outlook and difficulty agreeing on valuations for transactions.

“There’s a lot of headwinds,” said David Walker, a partner at law firm Latham and Watkins who focuses on private equity deals.

Job cuts at the largest US banks this year are on course to exceed 11,000 as Wall Street contends with the worst recruitment market since the 2007-08 financial crisis following a pandemic-era hiring binge.

Top banks like Goldman Sachs and JPMorgan, which raked in profits during the recent dealmaking boom, are wielding the axe. Goldman, top of the M&A advisory league table last year, is eliminating fewer than 250 jobs in fresh cuts across the bank, primarily at the senior level.

“We’re running the firm tighter and we’re preparing for a tougher environment,” Goldman president John Waldron warned at a conference this month. “Activity levels are definitely more muted.”

However, there were signs of optimism for dealmaking during the second quarter, up 23 per cent compared with the first, which was the slowest start to the year in a decade.

The second quarter pick-up has been helped by less traditional approaches to transactions.

“We’re seeing hostile bids, unsolicited [bids], topping bids, carve outs, spin-offs, you name it,” said Melissa Sawyer, global head of the M&A group at law firm Sullivan and Cromwell. “People are just having to get more creative in how they do things.”

The carve out of healthcare multinational Johnson & Johnson’s consumer unit marked the largest US initial public offering in almost 18 months.

And a hostile approach from the Swiss-based commodity trader Glencore to buy Canada’s Teck Resources for $23bn in April triggered one of the mining industry’s largest takeover battles in decades.

While Teck has repeatedly rebuffed Glencore’s advances, natural resource deals have otherwise been a rare bright spot in a slower M&A environment as companies focus on investing in metals necessary for the transition to cleaner energy sources and electric vehicles.

Groups ranging from traditional carmakers to a growing number of private equity firms are among the companies looking to invest in natural resources and cleaner energy, a shift from recent years.

“Everyone is looking to secure and produce supply in the short and medium term [in natural resources],” said Citi’s Barry Weir, who co-leads M&A across Europe, the Middle East and Africa. “We’re seeing a much broader universe of buyer.”

Another bright spot is healthcare, where deal volumes rose 35 per cent to $174.6bn in the first half compared with the same period last year as companies sought to refresh drug pipelines to compensate for a sharp fall in sales of pandemic-related products.

The largest contributor was Pfizer’s $43bn acquisition of Seagen, an oncology-focused biotech.

However, rising geopolitical tensions between Washington and Beijing are complicating dealmaking, as some western groups pull back from making investments in China.

Still, that is opening up other avenues for transactions as European companies turn to the US to expand.

“For the last decade there was a very strong focus on Asia including China,” said Birger Berendes, who co-leads Bank of America’s Emea M&A group.

“Now companies realise that the US may be really well positioned for the next decade in terms of growth and stability, so we have seen many European clients looking to expand in the US.”

With the US nearing a presidential election, that could also affect appetite for transactions. “We’re heading into an election year and it’s never clear in those periods of time how that impacts dealmaking or not,” added Krishna Veeraraghavan, a partner at law firm Paul Weiss.

But, despite the variety of factors slowing transactions, M&A volumes have held up compared with earlier prolonged slowdowns following the dotcom crash and the global financial crisis.

“If this is the trough right now, I’d take this as a trough in any cycle because activity just hasn’t stopped,” said Oliver Lutkens, co-head of advisory for the Emea region at BNP Paribas.